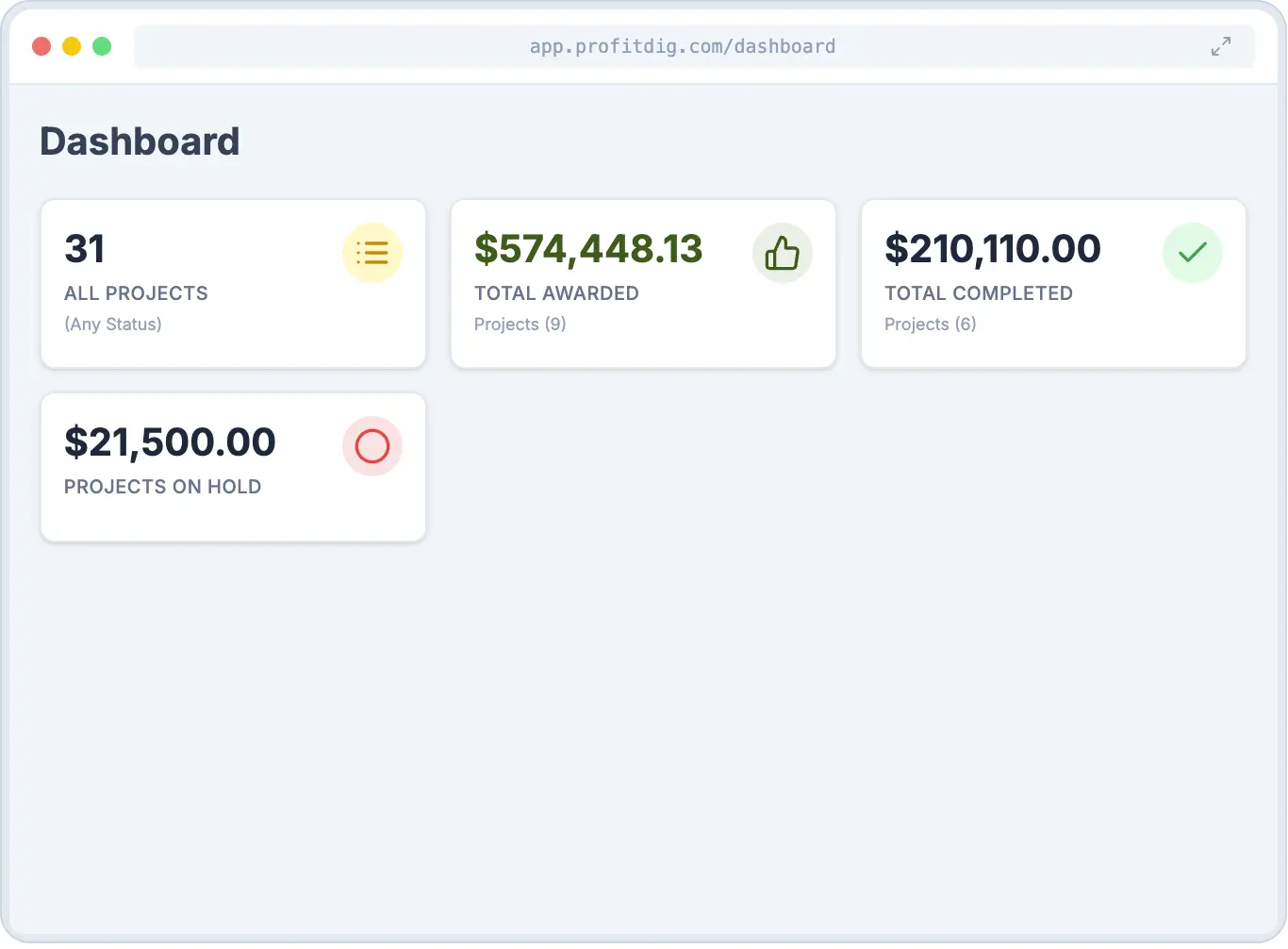

Know Your Margin

Before the First Bucket of Dirt Moves.

Bidding and job costing software built for sitework contractors.

Built by and for excavation, grading, and underground utility contractors. Bid jobs by the cubic yard and linear foot, track real costs against budget in real time, and stop finding out you lost money after the dirt is already moved.

How It Works

From your first number to the final invoice, ProfitDig keeps you in control the whole way.

Build your bid

Add line items by the cubic yard, linear foot, or unit. Your saved cost library fills in the numbers automatically.

Price it to win

Overhead, profit margin, tax, and bond are all calculated automatically. Know your number before the bid goes out.

Track every dollar in real time

As costs come in from the field, see exactly where you stand against budget. Job by job, line item by line item.

Stop rebuilding your grading & utility bid items every time.

Create, organize, and reuse your bid items and headers. Build a master database of your erosion control, grading, and underground utility items that speeds up every future proposal you create.

- Standardize your bidding language

- Quickly search and insert items

- Eliminate repetitive manual entry

Bid Items & Headers

Files

Measure your quantities straight from the plan. No manual scaling.

Upload the plan PDF, draw shapes over the areas and pipe runs you need to bid, and let ProfitDig do the math. Your measured quantities drop straight into the bid.

- Upload any plan PDF directly in the app

- Draw polygons for area, lines for pipe and conduit runs

- Export measured quantities straight to your bid

Materials

Group your pipe, aggregate, and erosion control materials once. Drop them into any bid.

Stop adding materials one by one. Group related materials together once, then drop the entire bundle into any line item. You save time and reduce the chance of missing something.

Any member can be promoted. Not tied to employee classification.

Build your crews once. Swap people and equipment on the fly.

Name your crews, assign employees and machines, and promote any member to acting foreman. When your roster changes mid-job, update it in seconds. Every cost change flows straight to your job report.

- Named crews with full equipment rosters

- Promote any employee to acting foreman

- Crew changes flow to job cost reports automatically

Quote excavation and underground utility work in minutes, not all weekend.

Stop reinventing the wheel for every proposal. Clone previous successful bids, use your saved item database, and generate professional PDFs instantly.

- Instant markup calculations

- One-click PDF generation

| Identifier | Quantity | Unit | Total | ||

|---|---|---|---|---|---|

| B Underground | $20,646.34 | ||||

| LI Standard Silt Fence | 1200 | [LF] | $4,839.08 | ||

Line Item Breakdown: 2001 | Grading & Excavation

Cost breakdown by material, labor, equipment, and other types

Profit Margin

12.00%

Overhead Rate

10.00%

Tax Rate

8.25%

Bond Rate

1.50%

| Equipment | Employees | Materials | |

|---|---|---|---|

| Raw | $8,240 | $5,690 | $1,050 |

| Profit | $989 | $683 | $126 |

| Overhead | $824 | $569 | $105 |

See where every dollar goes before the bid goes out.

Drill into any line item and see the exact split between equipment, labor, materials, and subs. Profit, overhead, tax, and bond are each broken out separately. No surprises after the job starts.

- Profit & overhead broken out per line item

- Equipment, labor, materials & subs at a glance

- Know your cost mix before you commit to a number

Keep a daily record of every job, every day.

Field and office teams log what happened on site each day. Record work performed, weather conditions, safety notes, visitors, and photos. Lock the entry when the day wraps, collect crew sign-offs, and export a signed Site Record PDF.

- Work, weather, safety, and visitor notes per day

- Each team member keeps their own dated entry

- Lock the day and collect crew sign-offs

- Export a printable Site Record PDF

Log time and expenses from a laptop, phone, or tablet.

You or your foreman can log hours, equipment time, and daily expenses from whatever's handy. A laptop at the office trailer or a phone from the cab both work fine. Cost data updates in real time the moment it's submitted.

See if that grading job is actually making money before it is too late to fix it.

Since ProfitDig is an online solution, your data is stored on a server, updated in real time. The minute one of your foremen records a timesheet or expense, that information is automatically available to you. Take the mystery out of dirt work project management and find out how you're really doing!

| Bid Item | Total | Materials | Employees | ||||||

|---|---|---|---|---|---|---|---|---|---|

| Cost | Budget | Diff | Cost | Budget | Diff | Cost | Budget | Diff | |

| 4060 - 3" PVC Water Line | $12,313 | $24,061 | $11,748 | $0.00 | $15,996 | $15,996 | $6,553 | $4,980 | -$1,572 |

| 2001 - Grading & Excavation | $8,940 | $9,500 | $560 | $2,100 | $2,400 | $300 | $4,200 | $3,900 | -$300 |

| 3001 - Storm Drainage | $5,210 | $4,800 | -$410 | $1,800 | $1,750 | -$50 | $2,100 | $2,400 | $300 |

Don't take our word for it.

"Since I’ve been using ProfitDig, my margins have increased and I have been making more money. It just works for me. It’s simplistic. I have used other estimating platforms in the past and ProfitDig is just better."

Simple, transparent pricing

No hidden fees. No long-term contracts. Cancel anytime.

Solo

- 1 User

- Unlimited Projects

- Profit & Loss Reporting

- Project Notes & File Storage

Team

- 3 Users

- Unlimited Projects

- Profit & Loss Reporting

- Project Notes & File Storage

Business

- 10 Users

- Unlimited Projects

- Profit & Loss Reporting

- Project Notes & File Storage

- Onboarding Assistance

From the Blog

Tips, updates, and field-tested advice for sitework contractors.

Pinned

PinnedJul 21, 2026

ProfitDig Summer Updates: Daily Diary, Bid Reconciliation, and Takeoff Enhancements

It has been a busy few weeks for the ProfitDig team since our major V3.5 release in June. We have been rolling out a steady stream of update...

Read more

Jul 28, 2026

What ChatGPT Gets Wrong About Construction Estimating

Artificial intelligence tools like ChatGPT have changed the way a lot of businesses operate. From drafting emails to summarizing contracts t...

Read more

Jul 14, 2026

How to Handle Change Orders Before They Become Arguments

Change orders are part of the job. The scope shifts, the customer adds something, or you uncover something nobody saw coming underground. Th...

Read more